Retirement is supposed to be a time for enjoying all you’ve worked for and finally relaxing. Yet nearly 40 percent of seniors may run out of money in retirement without a clear financial plan. Most people focus on saving money when they are young and miss the point that the real challenge comes later. Managing your finances as a senior means facing a mix of shrinking income, rising medical costs, and decisions about how to protect what you’ve built—and that’s where smart planning makes all the difference.

| Takeaway | Explanation |

|---|---|

| Create a personalized financial strategy | Tailor financial plans to individual goals, health, and risk tolerance to maximize effectiveness. |

| Prioritize income stability during retirement | Focus on developing sustainable income streams from various sources to ensure financial security. |

| Regularly assess your financial landscape | Conduct thorough evaluations of your income, expenses, and investments to stay on track with financial goals. |

| Mitigate healthcare cost risks | Plan for potential healthcare and long-term care expenses to prevent financial strain in later years. |

| Adopt a holistic approach to financial planning | Integrate different aspects of financial management to create a comprehensive plan that supports overall well-being. |

Financial planning for seniors represents a specialized approach to managing personal finances during retirement years, focusing on preserving wealth, ensuring income stability, and addressing unique financial challenges that emerge later in life. Unlike financial strategies for younger adults, senior financial planning requires a more nuanced and protective approach that considers diminishing earning potential, healthcare needs, and long term financial security.

The primary objective of financial planning for seniors is to create a comprehensive strategy that protects accumulated assets, generates sustainable income, and provides financial flexibility during retirement. This involves carefully evaluating current financial resources, anticipating potential expenses, and developing a robust framework that can adapt to changing personal and economic circumstances.

Key considerations in senior financial planning include:

Financial planning for seniors integrates multiple strategic components designed to provide comprehensive financial protection. According to National Institute on Aging, effective senior financial management typically encompasses retirement account optimization, investment diversification, estate planning, and healthcare cost mitigation.

Successful senior financial planning requires a holistic approach that balances immediate financial needs with long term security. Seniors must proactively assess their financial landscape, understanding that each individual’s requirements will differ based on personal circumstances, health conditions, and retirement goals. By developing a personalized and adaptive financial strategy, seniors can navigate their retirement years with greater confidence and financial stability.

Retirement represents a significant life transition where financial stability becomes paramount. While many seniors believe their savings will automatically sustain them, the reality is far more complex. Financial planning is not just a recommendation but a critical necessity that determines quality of life, independence, and peace of mind during retirement years.

The financial landscape for seniors is fraught with potential challenges that can quickly erode accumulated wealth. Inflation, unexpected medical expenses, market fluctuations, and increased longevity create substantial financial pressures that require strategic planning.

The following table outlines the main financial risks that seniors face during retirement and their potential consequences, helping readers understand what challenges financial planning seeks to address.

| Financial Risk | Description | Potential Consequences |

|---|---|---|

| Unpredictable healthcare costs | Unexpected medical expenses and rising healthcare prices | Large out-of-pocket costs, reduced savings |

| Potential long-term care expenses | Need for assisted living or in-home care | Rapid depletion of retirement funds |

| Market volatility affecting investments | Fluctuations in investment value | Loss of wealth, reduced income |

| Reduced earning potential | Limited capacity to generate new income in retirement | Increased reliance on savings |

| Increased living expenses | Growth in housing, food, and other daily costs | Difficulty maintaining standard of living |

| According to Employee Benefit Research Institute, approximately 40% of seniors risk running out of money during retirement if they do not implement comprehensive financial strategies. |

Key financial risks seniors face include:

Effective financial planning enables seniors to maintain autonomy and make proactive choices about their lifestyle. The goal is not merely survival but preserving dignity and options. By anticipating potential financial challenges and creating robust contingency plans, seniors can protect themselves from becoming financially dependent on family members or government assistance programs.

Beyond mere financial survival, comprehensive retirement planning allows individuals to pursue personal goals, engage in meaningful activities, and potentially support causes or family members they care about. A well-structured financial plan transforms retirement from a period of potential anxiety to an opportunity for continued personal growth and fulfillment.

Financial planning for seniors requires a comprehensive approach that addresses multiple interconnected aspects of financial management. Effective retirement financial strategies go beyond simple savings, integrating sophisticated planning techniques that protect and optimize financial resources during later life stages.

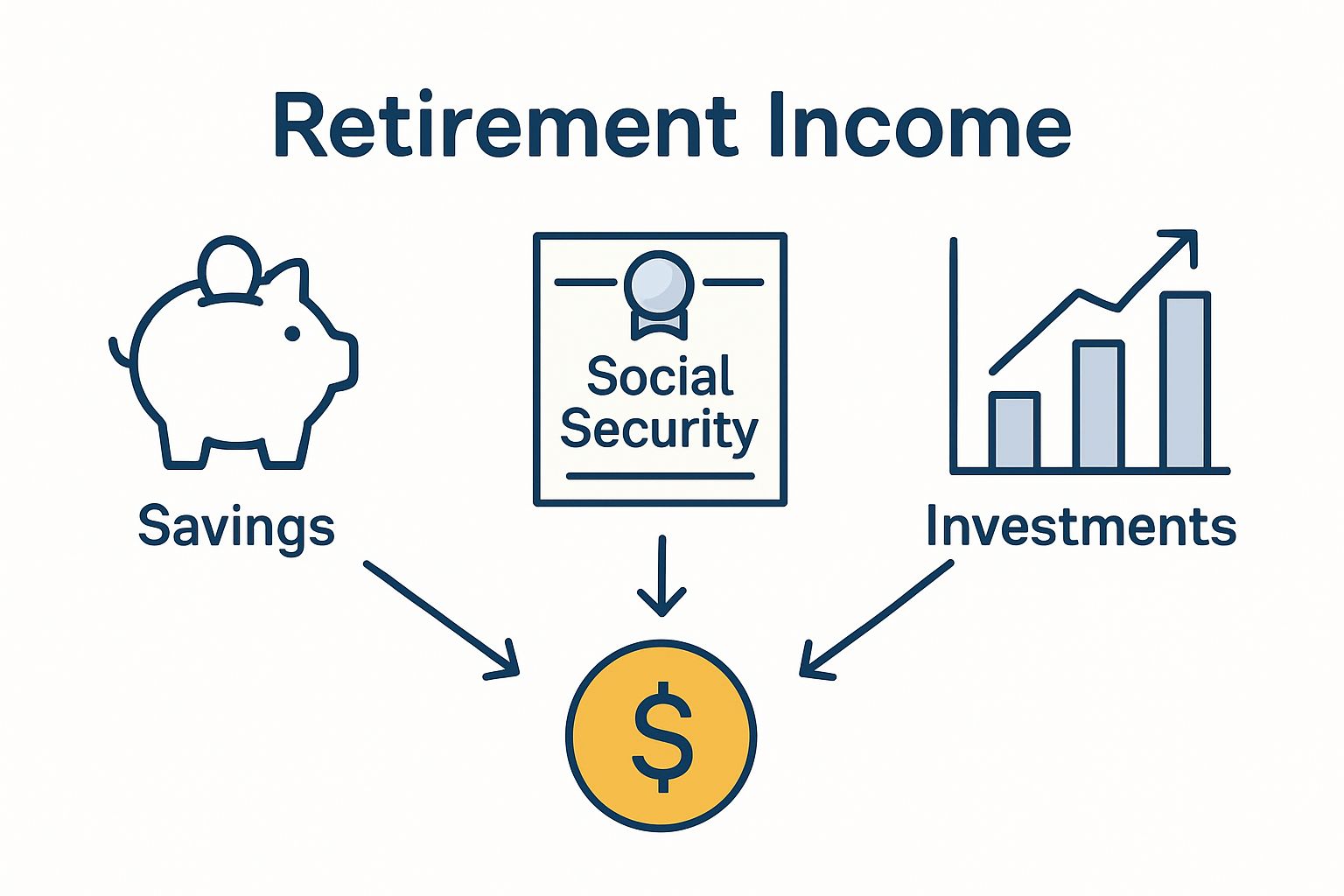

Retirement income planning involves creating sustainable financial streams that can support seniors throughout their retirement years.

This complex process requires careful analysis of potential income sources, including Social Security benefits, retirement account distributions, pension plans, and potential part time work opportunities. According to Social Security Administration, understanding and maximizing Social Security benefits can significantly impact overall retirement income stability.

This complex process requires careful analysis of potential income sources, including Social Security benefits, retirement account distributions, pension plans, and potential part time work opportunities. According to Social Security Administration, understanding and maximizing Social Security benefits can significantly impact overall retirement income stability.

Key retirement income considerations include:

Prudent investment management becomes crucial during retirement, requiring a strategic shift from growth oriented to preservation focused approaches. Seniors must carefully balance investment portfolios to generate reasonable returns while minimizing potential market risks. This involves diversifying investments across different asset classes, maintaining appropriate risk levels, and regularly rebalancing portfolios to align with changing financial needs and market conditions.

The primary goal of senior investment management is not aggressive growth but consistent, stable returns that can support ongoing living expenses while protecting accumulated wealth from potential economic downturns. Flexibility and continuous reassessment are fundamental to maintaining a robust financial strategy that adapts to evolving personal and economic circumstances.

Approaching financial planning as a senior requires a strategic, thoughtful methodology that acknowledges the unique complexities of retirement financial management. Successful financial planning is not a one time event but an ongoing process that demands continuous attention, adaptability, and proactive decision making.

The initial step in senior financial planning involves conducting a thorough and honest evaluation of current financial circumstances.

This table summarizes the key steps involved in conducting a comprehensive financial assessment for seniors, clarifying each step and its purpose within the planning process.

| Step | Purpose |

|---|---|

| Document all income streams | Identify all consistent and potential sources of retirement income |

| Calculate current and future expenses | Understand necessary spending to maintain lifestyle |

| Review existing insurance coverage | Ensure protection against unexpected health or property costs |

| Evaluate current investment portfolios | Assess asset mix and risk exposure for retirement needs |

| Understand potential healthcare costs | Anticipate and prepare for future medical expenses |

| This comprehensive assessment goes beyond simple balance sheet calculations, requiring seniors to critically examine their income sources, existing assets, potential liabilities, and projected future expenses. Federal Deposit Insurance Corporation recommends seniors perform regular financial check ups to ensure their strategies remain relevant and effective. |

Key elements of a comprehensive financial assessment include:

Financial planning is inherently personal, necessitating strategies tailored to individual circumstances, goals, and risk tolerances. Seniors must recognize that a one size fits all approach is ineffective. This personalized strategy should integrate multiple financial considerations, including tax planning, estate management, potential long term care needs, and sustainable income generation.

Successful financial planning requires seniors to remain flexible, continuously educate themselves about changing financial landscapes, and potentially seek professional guidance from certified financial advisors who specialize in retirement planning. By maintaining a proactive and adaptive approach, seniors can create a robust financial framework that provides security, independence, and peace of mind throughout their retirement years.

Financial planning transforms theoretical strategies into tangible actions that directly impact seniors’ quality of life. Real-world applications bridge the gap between financial concepts and practical daily living, enabling seniors to navigate complex financial landscapes with confidence and strategic precision.

One of the most critical real-world applications of financial planning involves managing potential healthcare expenses. According to National Institute on Aging, healthcare costs represent a significant financial challenge for seniors, requiring sophisticated planning and proactive resource allocation.

Practical healthcare financial strategies include:

Effective financial planning directly influences lifestyle sustainability, enabling seniors to maintain their desired standard of living while protecting accumulated wealth. This involves creating flexible income streams that can adapt to changing economic conditions and personal circumstances. Seniors must balance immediate financial needs with long-term preservation strategies, considering factors such as inflation, potential market fluctuations, and unexpected life events.

Successful real-world financial planning goes beyond mere number crunching. It requires a holistic approach that considers emotional well-being, personal goals, and the ability to make informed financial decisions that provide both security and the freedom to enjoy retirement years with dignity and peace of mind.

Taking control of your financial future in retirement often means rethinking your living situation. The article highlighted how essential it is for seniors to preserve wealth, minimize unexpected expenses, and maintain independence. Finding a trusted partner for moves or downsizing can relieve financial and emotional stress—especially when every decision impacts your long-term stability.

If you are looking for secure, reliable support during this next chapter, US Pro Logistics is ready to help. We specialize in senior moves, offering flexible solutions that protect your belongings, save you time, and offer peace of mind throughout the transition. Discover how our dedicated team can simplify your relocation so you stay focused on your retirement goals. Visit US Pro Logistics today to request your personalized quote and start making confident choices for your future. Act now and take the next step toward safer, worry-free living.

Financial planning for seniors is crucial for maintaining financial independence and stability during retirement. To start, assess your current financial situation and clarify your long-term goals to ensure your plan aligns with your lifestyle needs.

Begin by evaluating your unique circumstances, including income sources and expected expenses. Create a customized strategy that addresses your specific needs and risk tolerance, adjusting it as your situation changes over time.

To support yourself during retirement, explore various income sources such as Social Security, pensions, and any potential part-time work. Aim to balance guaranteed income streams with variable income options to ensure consistent funding.

Healthcare costs can significantly impact seniors, so it’s essential to evaluate your insurance coverage and plan for potential out-of-pocket expenses. Review your current healthcare plans and set aside dedicated savings for medical emergencies or long-term care needs.

To safeguard your investments, focus on creating a diversified portfolio that balances growth with risk management. Regularly review and adjust your investment strategy to respond to market changes, ensuring you maintain a consistent return that aligns with your retirement goals.

Reassess your financial plan at least annually or when significant life changes occur, such as health issues or changes in income. Schedule regular financial check-ups to adapt your plan based on your evolving situation and keep your retirement goals on track.

USDOT 3664256 This number is required for any company that operates commercial vehicles in interstate commerce (across state lines). It helps identify and track the safety performance and compliance of transportation companies.

MC 1268070 This number is specifically for companies involved in the transportation of goods or passengers for hire across state lines. It’s necessary for carriers operating in the moving industry and ensures they are authorized to operate as interstate carriers.